Key events this week – US tariff announcement, US non-farm payrolls & ISM surveys, Fed Chair Powell speech, RBA meeting, global S&P PMI’s Mar

Recap from last week: US inflationary pressures persist amid slowing growth

US data last week reflected a tension between signs that inflation pressures are persisting and signs that growth is slowing. Announcements of auto tariffs last week, ahead of a broader tariff announcement due this week, are fuelling consumer and business expectations of inflation in the near-term, and driving sentiment lower. At the same time, there are signs that US growth is slowing through Q1.

Last week’s reports underscored persistent inflation pressures and rising inflation expectations among households and businesses. Firstly, US PCE price inflation for Feb confirmed this trend, with headline inflation steady at +2.5% but the monthly rate slightly firmer. More concerningly, core PCE inflation rose to +2.8%, driven by increases in both core goods (now no longer deflationary) and core services. This suggests that progress on disinflation may be stalling.

Secondly, a further weakening in sentiment was influenced by expectations of rising inflation and this was broadly reflected in both consumer and business surveys last week. The consumer sentiment reports last week were consistent; there is a divergence between relatively stable, albeit low, sentiment readings for current conditions contrasting with a notable weakening in the outlook for personal finances, business conditions, unemployment, and inflation. Consumers are saying ‘Things aren’t great now, but the outlook is causing notable unease’.

Among businesses, the US S&P prelim PMI showed an improvement in private sector output in Mar – but conditions were mixed. A rebound in services output more than offset the marked fall in manufacturing output. There was a question about the durability of the services expansion. Rising input costs were a key theme of the report, highlighting that cost pressures had intensified across both sectors, but especially in manufacturing. While manufacturing firms were passing through these higher input costs, the report noted that concerns over sluggish demand were hampering service firms’ ability to pass on higher costs – despite the improvement in services activity output this month. The fall in the business outlook was led by concerns over policy initiatives, while firms also cited weakening customer demand.

Amid this persistent inflation, last week also brought further evidence of slowing growth. Business concerns over slowing demand were reflected in Feb’s slower-than-expected personal spending growth. Personal spending growth did rebound in Feb, but by less than expected, while the fall in spending for Jan was revised lower. In real terms, personal spending increased by a modest +0.1% in the month. It was notable that spending on services fell by -0.1% in real terms in Feb, led by a -1.4% fall in food services & accommodation – the third weak month in a row. Spending on goods did rebound in Feb, but only partially offset the fall in goods spending in Jan. The effect of the Auto tariff announcement last week may boost personal spending in the short term as demand may be pulled forward ahead of the tariff.

A relatively bright spot in the data was the personal income report for Feb – suggesting that, overall, the footing of the consumer/households remained solid, despite the dour outlook. Total personal income growth accelerated in Feb by more than expected – although growth was led mostly by an increase in “other” government transfer receipts (not a sign of economic strength, but there was no increase in unemployment insurance payments), however, employee compensation growth also accelerated. The other bright spot remains the relatively low and stable initial jobless claims – a near-term indicator suggesting that labor market conditions have not deteriorated more recently.

Zooming out to overall US economic growth, the latest estimate of GDP tracking for Q1 paints a similar picture of deceleration. The Atlanta Fed GDP nowcast for Q1 slowed further this week, now indicating an adjusted -0.5% growth rate for the quarter, with another month of data remaining to close out the quarter. While domestic demand (excluding external factors) remains positive, its pace has also moderated.

Outlook for the week ahead; US tariff announcement, US non-farm payrolls & ISM surveys, Fed Chair Powell speech, RBA meeting, global S&P PMI’s Mar

The focus this week is likely to remain firmly on the tariff announcement expected on 2 Apr and its implications for growth and inflation. The details will be important including the scope of tariffs, expectations of further tariff announcements, and general timing for actions.

On the data flow, the US non-farm payrolls and labor market report for Mar will take center stage this week and will be crucial for assessing consumer fundamentals and implications for the consumption outlook. There will also be several important Fed speeches this week, including Fed Chair Powell, Vice Chair Jefferson, and Governor Cook, all speaking about the economic outlook.

Key factors to watch this week;

US non-farm payroll growth is expected to slow in Mar.

Non-farm payrolls are expected to increase by +139k in Mar, edging down from +151k in Feb. As always, the direction of revisions will be important.

The unemployment rate is expected to be unchanged at 4.1% in Mar.

The average workweek is expected to increase to 34.2 hours/week.

Job openings for Feb are expected to slow only slightly to 7.73m from 7.74m in Jan.

The Challenger Job Cut Announcement survey for Mar will be closely watched. The Feb report showed a marked increase of 172k job cut announcements led by, but not limited to, government job cuts.

Initial claims are expected to edge slightly higher to +227k for the week ending 29 Mar.

Other US data will also provide input into the growth trajectory for the final month of Q1;

The US ISM surveys for Mar are expected to show a slowdown in manufacturing activity while services activity is expected to continue expanding at a moderate pace.

Factory Orders for Feb are expected to increase by +0.5%, down from +1.7% in Jan.

There will be several US Fed speeches this week. The key speeches will be US Fed Chair Powell (Fri), Vice Chair Jefferson, and Governor Cook, all speaking on the economic outlook.

The RBA will meet this week and is expected to keep policy settings unchanged with the cash rate target at 4.10%. At the prior meeting, the RBA Board reduced the cash rate for the first time in this cycle, noting increased confidence in inflation progress. Yet, the Board remained cautious on the prospects of further easing. Guidance from this meeting will be important.

Other important data out this week includes;

The latest ECB minutes of the latest meeting.

The prelim Euro area CPI for Mar is expected to ease to +2.2% over the year and remain unchanged at +0.4% over the month. Core CPI is expected to ease to +2.5% over the year in Mar, down from +2.6% in Feb.

Canada’s labour market report for Mar will be important from the perspective of gauging progress on the current recovery and any impact so far from trade and tariff announcements. Employment growth is expected to remain low at a net +9.9k for the month. The unemployment rate is expected to increase to 6.7%.

The broader suite of global PMIs for Mar will be released this week. The flash PMIs for Mar showed broadly that services output had continued to grow and build on the first two months of the year, whereas manufacturing output continued to contract – and to a greater extent than in the prior two months.

This week, the US Treasury will auction and/or settle approx. $688bn in ST Bills, Notes, Bonds, and TIPS, raising $121bn in new money.

QT this week: Approx $21bn of ST Bills, Notes, and Bonds will mature on the Fed balance sheet and will be reinvested. Approx $19bn of Notes & Bonds will be redeemed and roll off the fed balance sheet.

More detail (including a calendar of key data releases) is provided in the briefing document – download the pdf below:

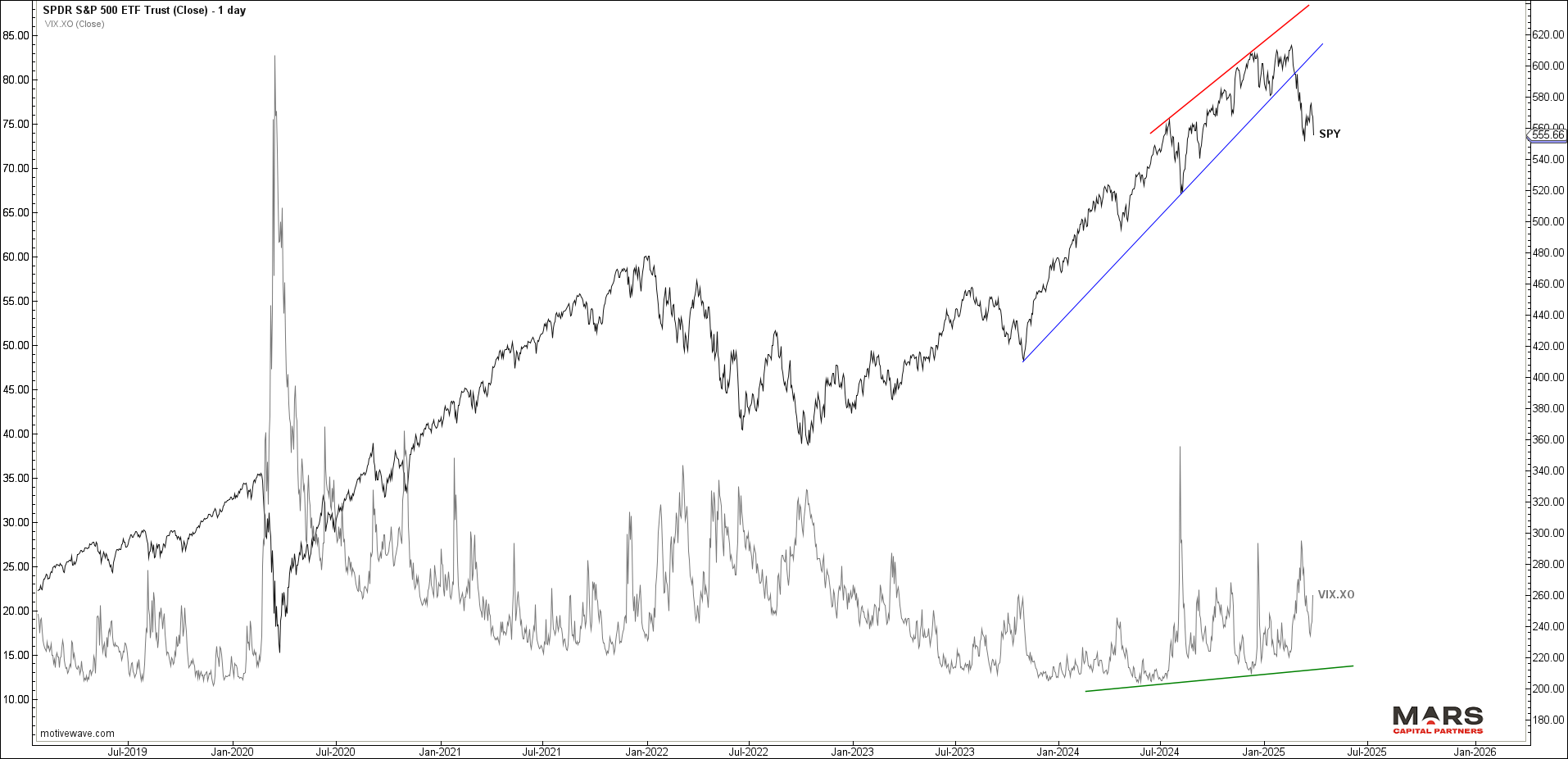

Last week, equities extended higher as expected in a counter-trend rally into overhead resistance before reversing sharply lower. The question is whether the rally was “all” or “part” of a wave B counter-trend rally. The impulsive nature of Friday’s decline warns of an immediate red wave C decline towards big picture targets. The alternate is a more complex green wave B if bulls can hold recent swing low support. The equity markets remain bearish from a big picture perspective until proven otherwise.

Rates and the US$ are attempting to reverse lower to help confirm our bearish outlook as this risk off environment takes hold. The shorter end of the bond market in particular appears bullish as we look for a 5th wave extension higher. The Euro held key support and is attempting to reverse higher to help maintain our bullish outlook. Gold pushed to new ATH’s as expected but the rally is very extended as we look for evidence of a tradable top. Trump’s tariffs continue to weigh on markets as the economic outlook remains uncertain.

Equity Markets – Bear reversal

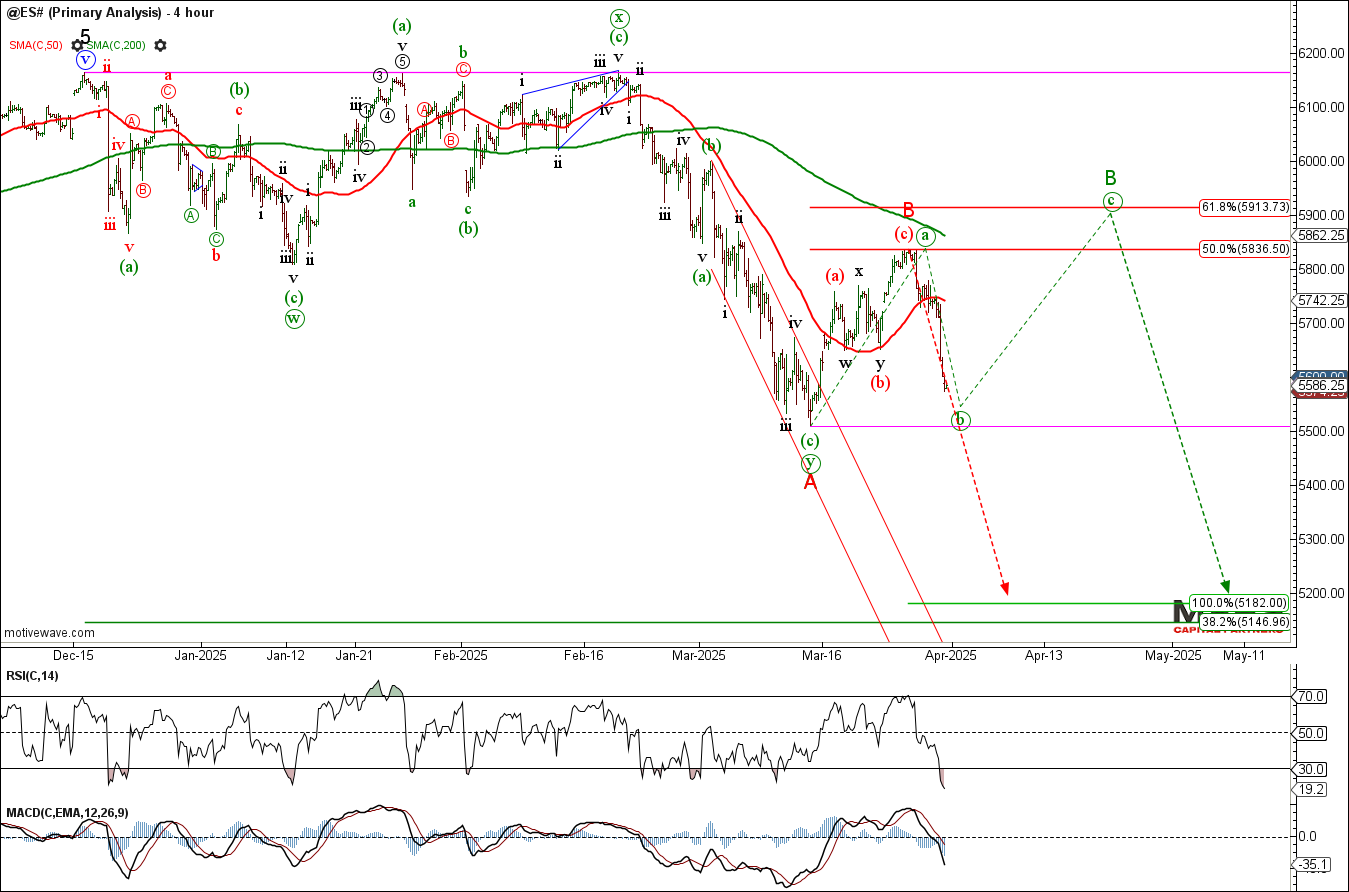

To the equity markets and the benchmark SPX / ES extended higher for a counter-trend wave (c) rally before reversing sharply lower as expected. The impulsive nature of last week’s decline warns that red wave B is complete and a strong wave C decline is underway. The alternate is a more complex green wave B counter-trend rally if bulls can hold recent swing low support. Either way, the recent counter-trend rally helped confirm our bigger picture bearish outlook with wave (4) targets lower towards the 5150 area. Bearish now or bearish later…

ES DailyES H4

ES traders flipped net short.

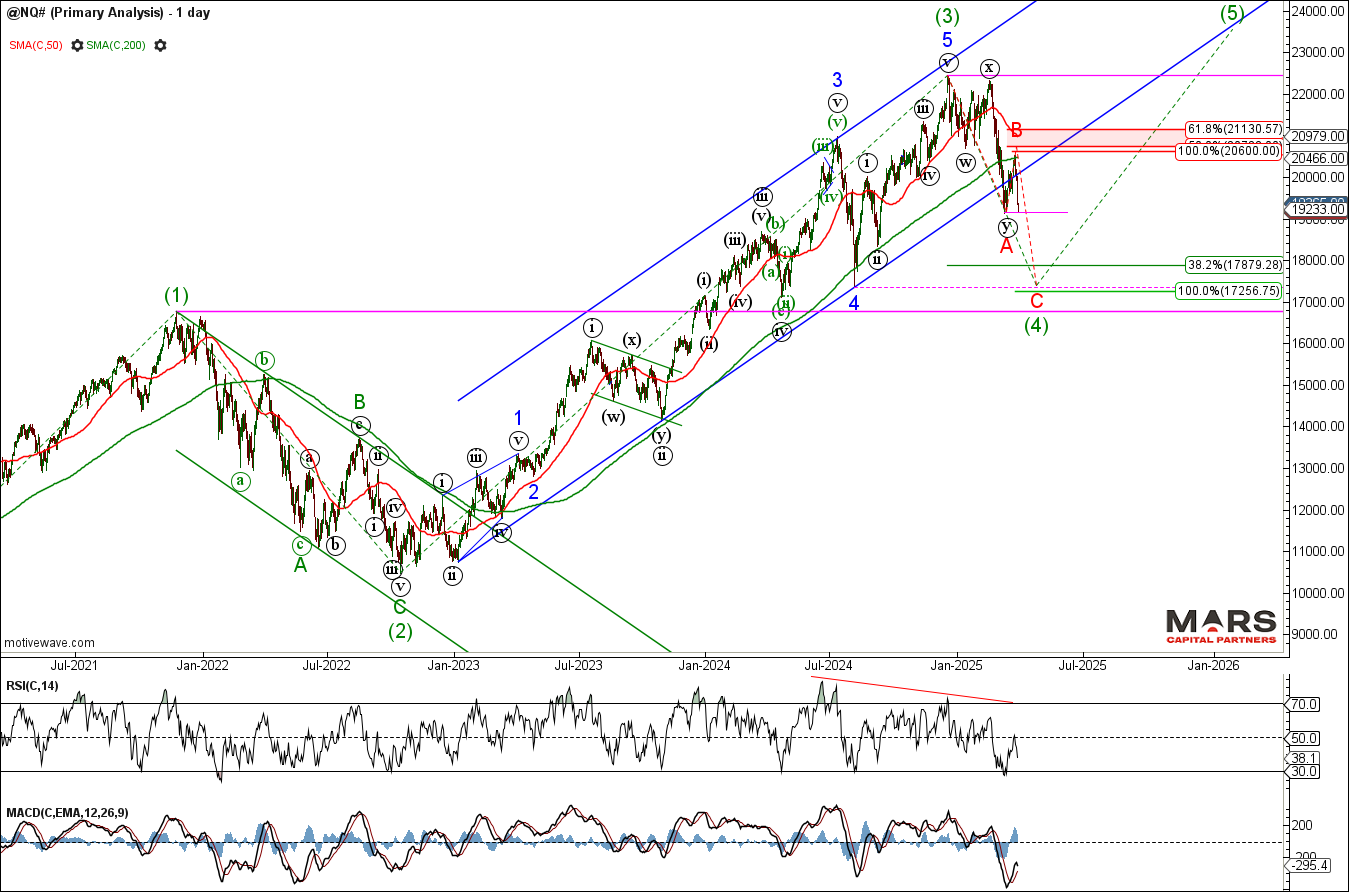

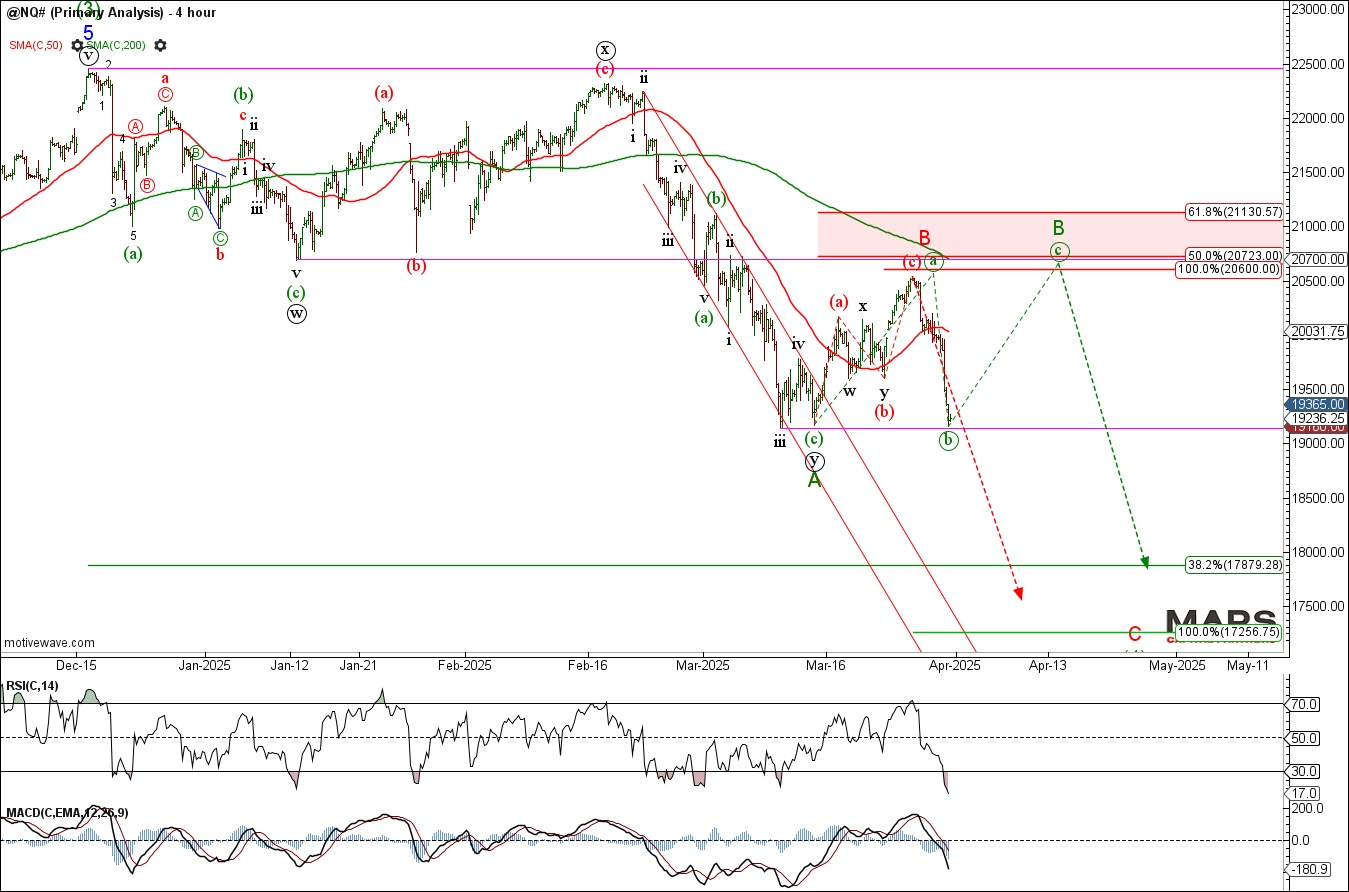

The Nasdaq / NQ also extended higher in a counter-trend rally before reversing sharply lower. While there are enough waves in place to complete red B, bears need to break recent swing lows and continue its impulsive decline to help confirm wave C down. The alternate is a more complex green wave B counter-trend rally if bulls can hold near term support. Either way, the bigger picture trend remains bearish until proven otherwise as we look for wave (4) down towards targets in the 17250 area.

NQ DailyNQ H4

The Russell 2000 / RTY reversed sharply lower while below key overhead resistance as expected. The question is whether the rally completed green wave (a) or “all” of red 4 with wave 5 down on deck. The structure remains bearish while below the wave 1 overlap in the 2172 area as we look for confirmation of a bigger picture bearish decline.

RTY DailyRTY H6

The VIX reversed sharply higher from 200 day sma support but it remains range bound from a big picture perspective. This consolidation is consistent with a bigger picture wave (4) correction in the equity markets. No edge here as the range racing continues and Trump threatens a trade war. The response in the VIX has been muted so far.

VIX DailySPY / VIX Daily

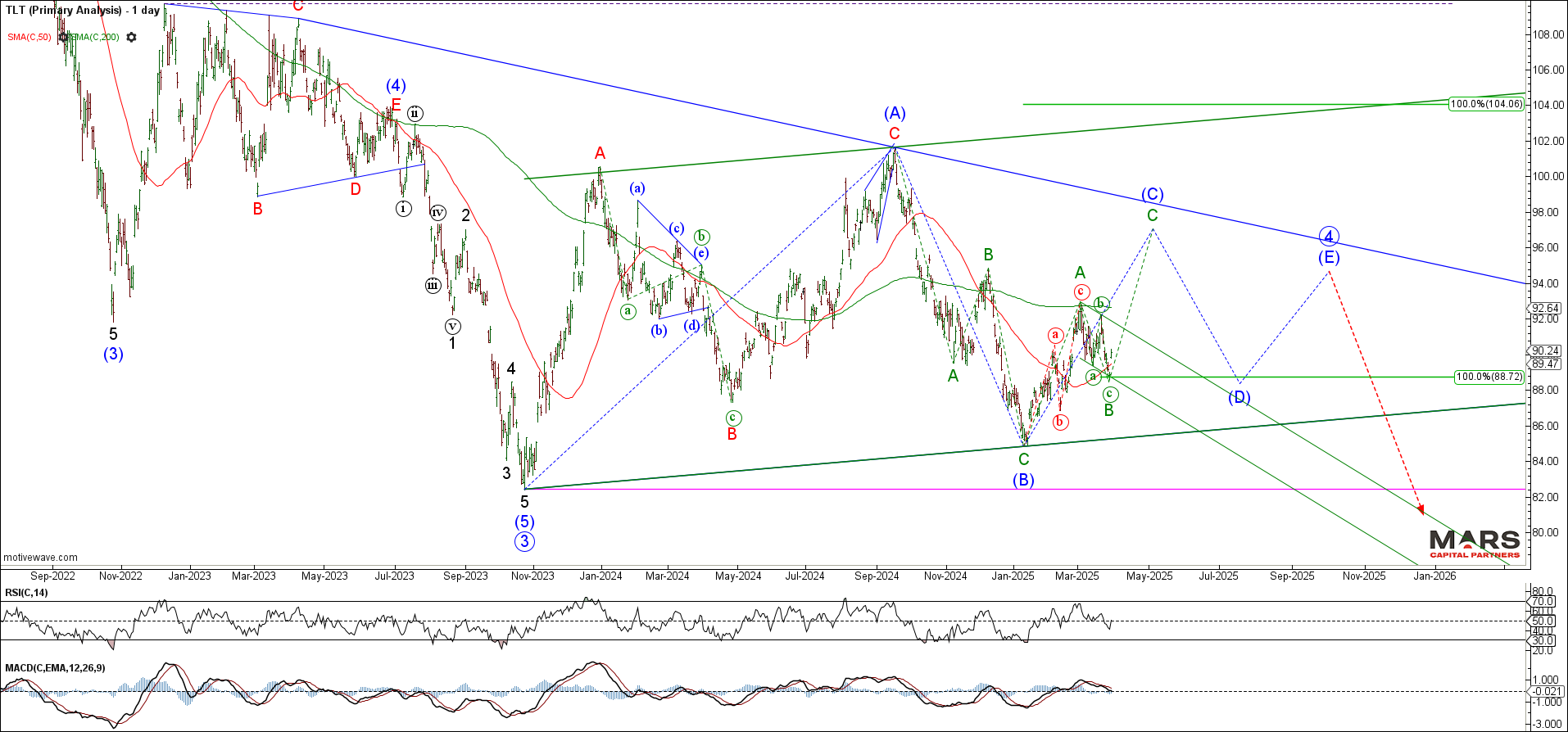

Bond Markets – Breaking higher?

To the bond markets and the TLT declined in 3 waves of equality before reversing higher late last week. The TLT is likely trapped within a big picture triangle but bulls need to clear overhead resistance at the 200 day sma to help confirm more bullish potential. It remains range bound within a big picture consolidation until proven otherwise.

TLT Daily

The 30yr / ZB only shows 3 waves up and 3 waves down so far but has the potential for a break higher in wave C of (C). Bulls need to clear 200 day sma resistance to open the door to a larger rally. Likely limited upside given the corrective nature of the initial rally within a big picture triangle.

ZB Daily

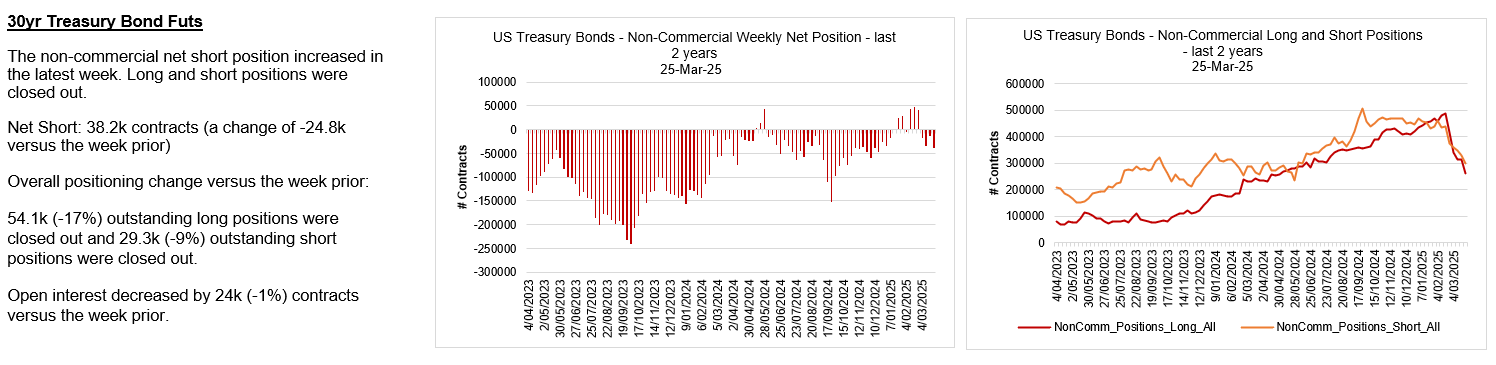

Bulls and bears are exiting long bonds en mass.

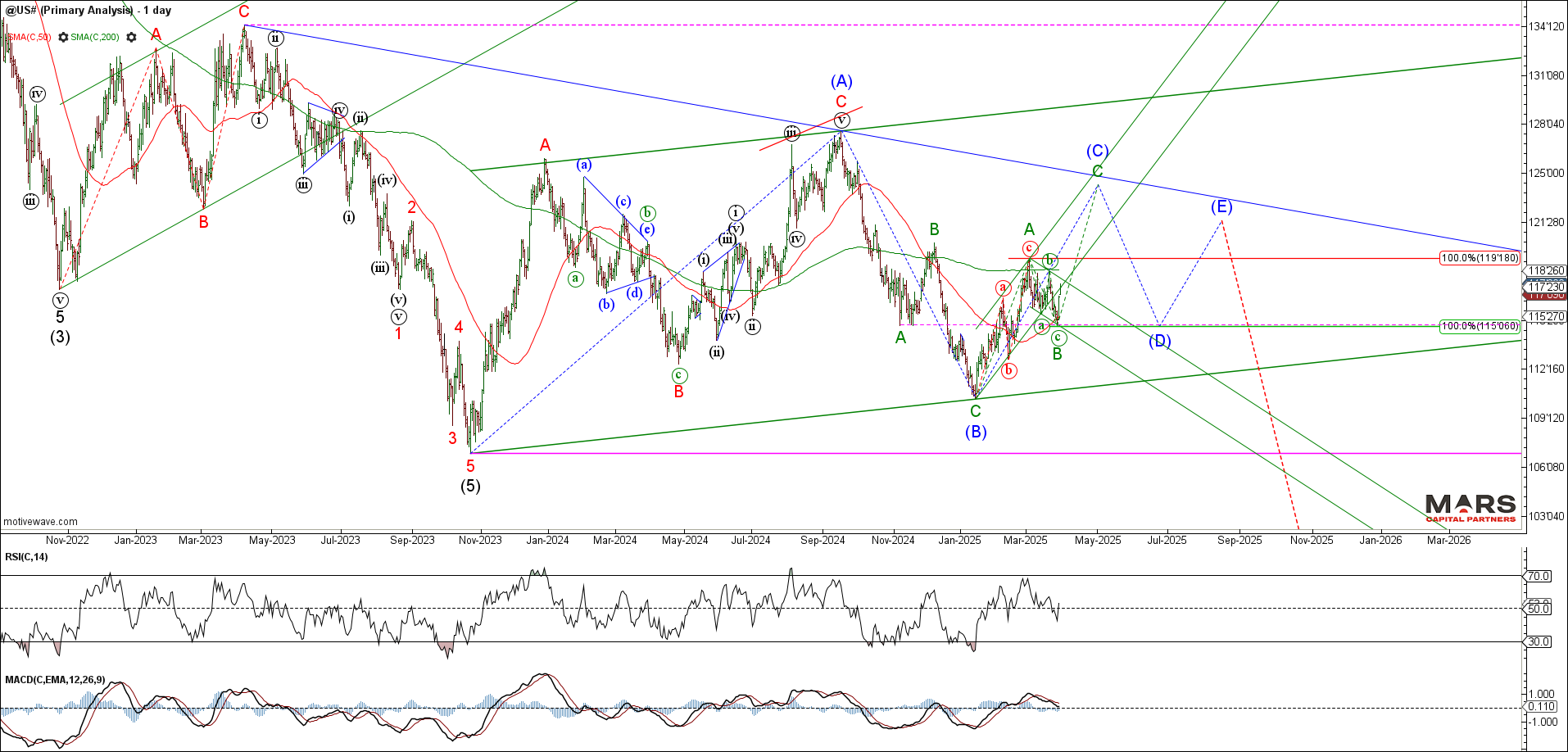

The US10yr / TY held overlap support and rallied strongly late last week to help set up a 5th wave rally. Bulls need to clear 112 overhead resistance to open the door to a bigger picture wave (C) higher. We continue to see this rally as part of a larger degree correction. Despite being range bound, the outlook remains higher for a bigger picture wave (C) rally.

TY DailyTY H4

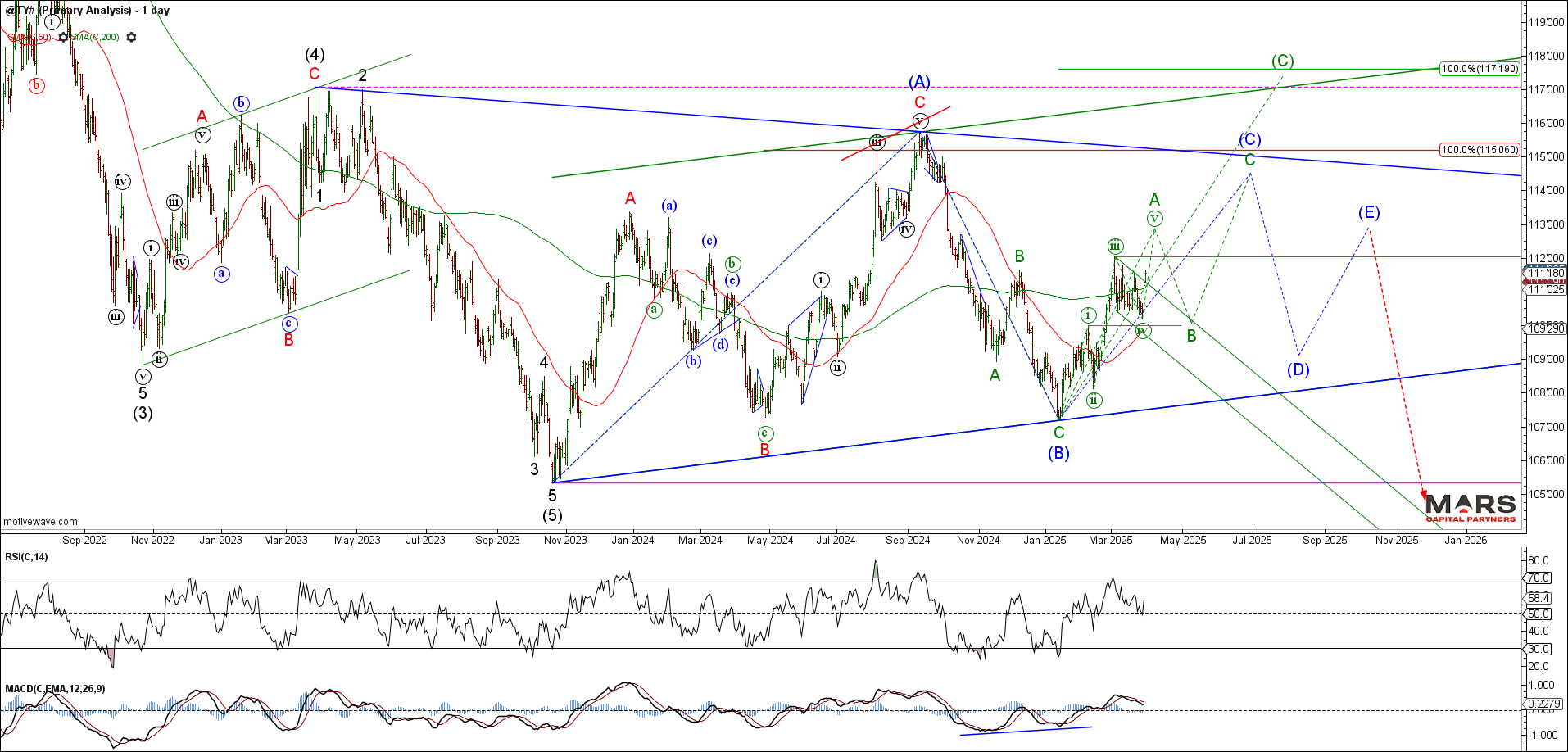

The US5yr / FV also held our near term support and rallied strongly late last week. Bulls need to clear overhead 118’20 resistance to help confirm 5 waves up from the lows and open the door to a bigger picture wave (C) rally. Bonds remain range bound from a big picture perspective with upside potential in the 112 area.

FV DailyFV H4

Both rates and the US$ would look better with downside extensions to keep the bear trends intact.

TNX / DXY Daily

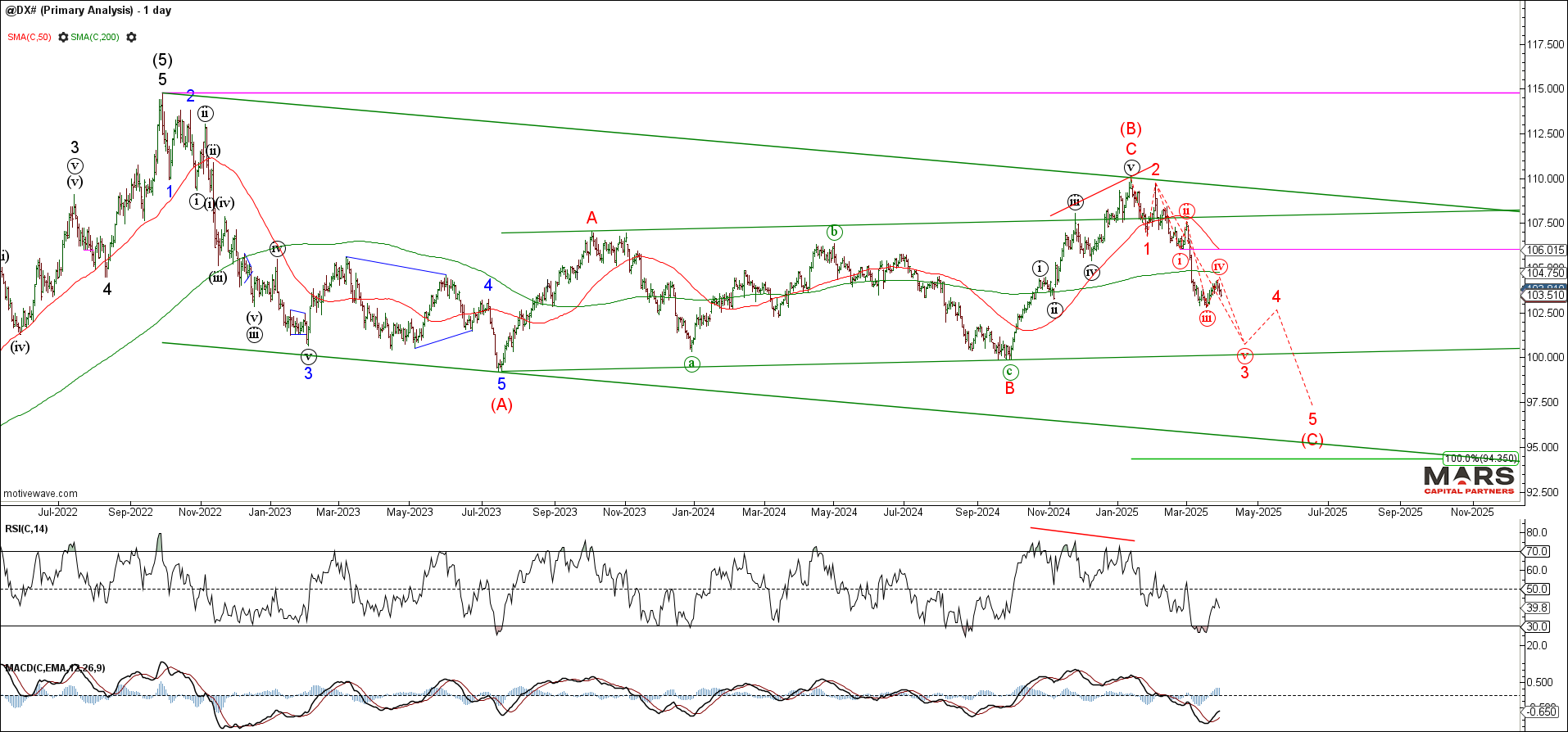

FX Markets – DXY turning lower?

To the FX markets and the DXY is attempting to turn lower for what we expect to be part of a bearish wave (C) decline. The structure remains bearish while below the key 106 wave (i) overlap. Ideally, we’d like to see a downside continuation this week to help maintain the bear trend with bigger picture targets in the 95 area.

DXY DailyDXY H4

The Euro held near term support at the 200 day sma and is attempting to rally up off these lows. The near term rally is not yet clearly impulsive and needs to clear 1.0950 resistance to help confirm our bullish outlook. Bulls need to hold the line here. Trade back below the 1.0533 wave (i) overlap invalidates the bull case.

EURUSD DailyEURUSD H4

Euro traders have flipped net long.

The USDJPY reversed sharply lower from the 50 / 200 day sma resistance but the decline appears corrective. While the potential remains for an extension lower towards trend support in the 144-145 area, there is no clear directional trend. Best to avoid until we see a clearly impulsive trend develop – range racing with no edge.

USDJPY Daily

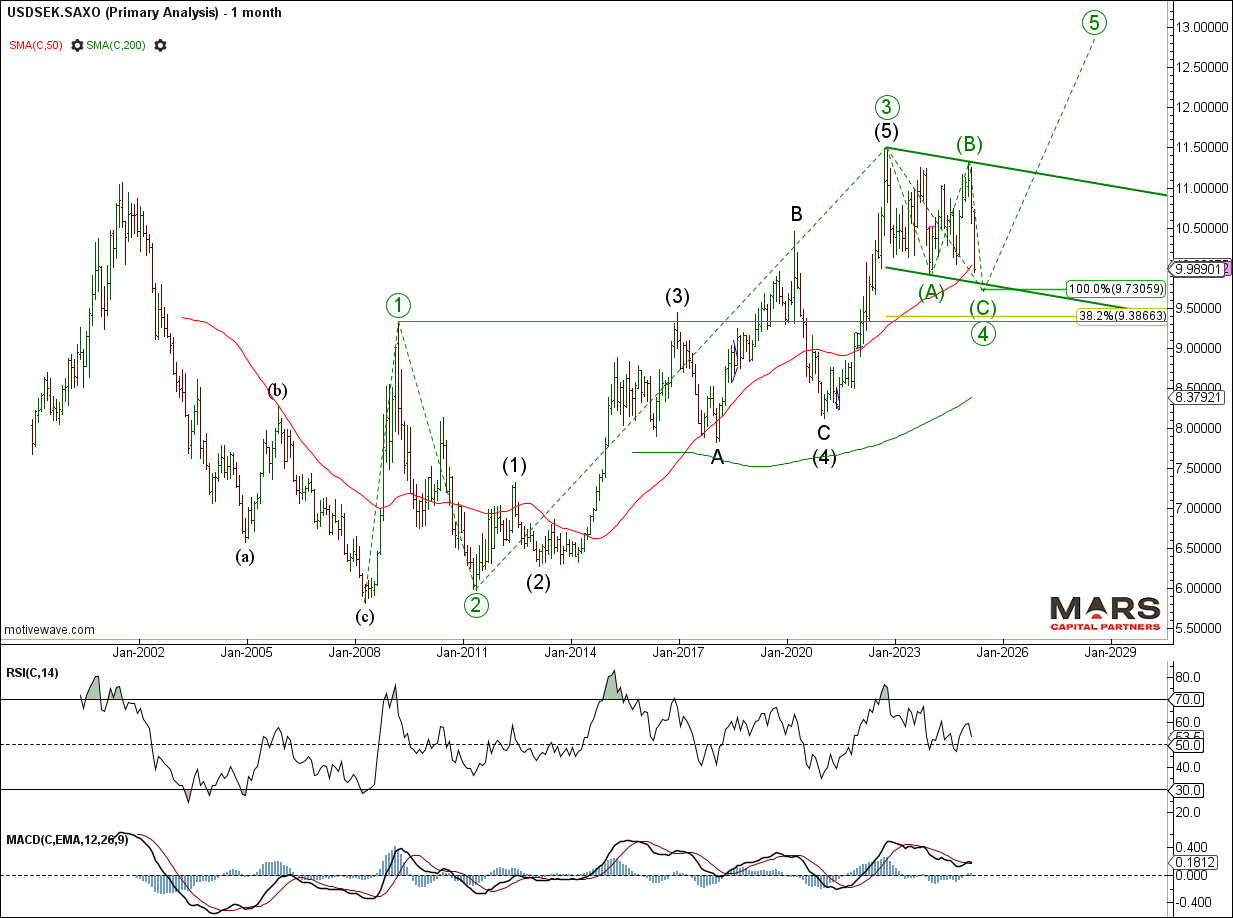

The USDSEK is fast approaching big picture support in the 9.73 area. The decline from the 2022 highs appears to be a 3-3-5 “Flat” correction within a larger bull trend. Ideally, we’d like to see a 5 wave decline that terminates in the 9.73 area before evidence of a bullish reversal. Given the bearish outlook for the US$ across the board, it’s best to await evidence of a bullish reversal before considering longs. Critical overlap support remains lower towards the 9.32 area.

USDSEK DailyUSDSEK Monthly

Commodity Markets – Gold new ATH’s

To the commodity markets and Gold pushed to new ATH’s in what appears to be a 5th wave blow-off top. While there are enough waves to complete wave (v) of 5 of (3) up, there is no evidence yet of a tradable top. Bears need to break the series of higher highs and higher lows to help confirm a change in trend. Too early to call.

Gold DailyGold H4

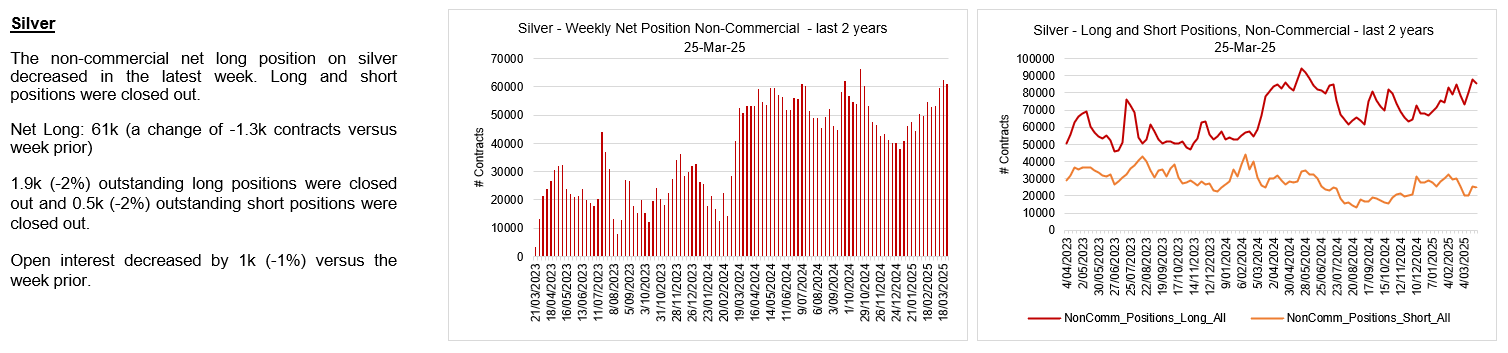

Silver is testing major swing highs as we look for a final wave 5 rally. There is no evidence of a tradable top as it continues to wedge into the highs. We are wary that this latest rally is potentially an ending wave so buyer beware as it pushes to new cycle highs. The fake-out new ATH’s in Copper is a warning to all.

Silver 2D

Silver bulls pressing into the highs.

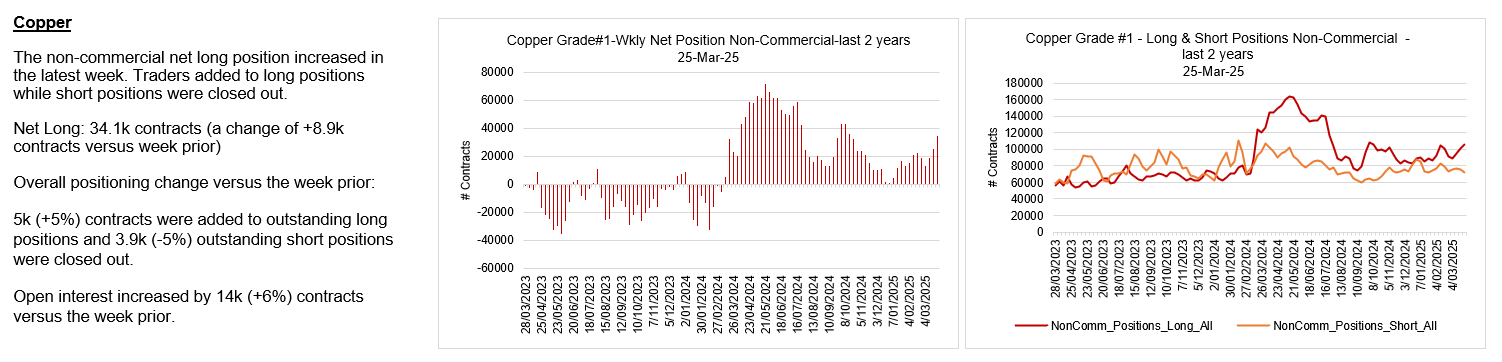

Dr Copper pushed to new ATH’s but reversed sharply lower as warned. Bears need to see downside follow through this week to help confirm a potential top. An impulsive decline that breaks overlap support in the 4.83 area would be the first indication of a potential change in trend. Trade above last week’s highs likely sees a 5th wave extension higher. Near term inflection.

Copper WeeklyCopper H4

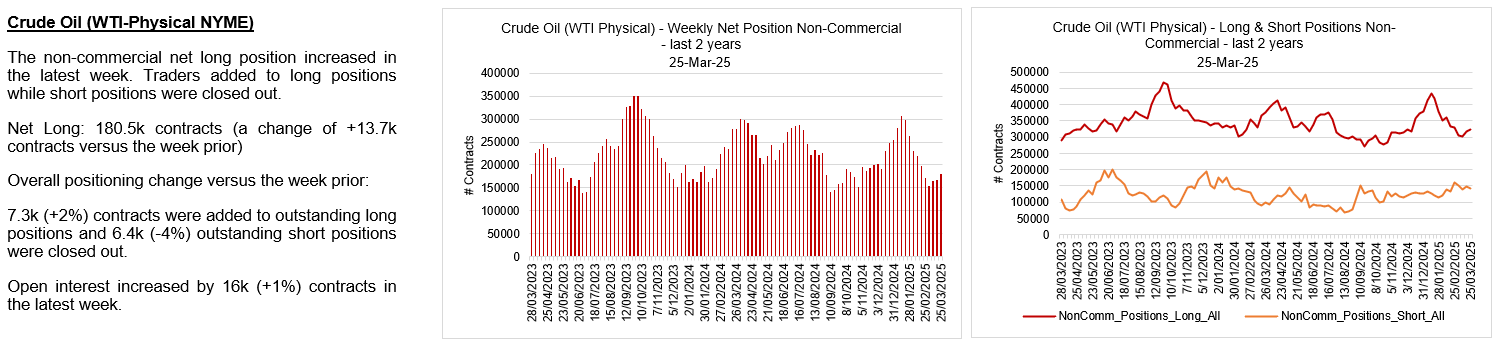

Crude Oil continues to hold shelf support but would still look best with a final push lower to potentially complete wave 5 of (C) down. The alternate continues to be a triangle wave (B) consolidation if bulls can break up from this support. Two-way risks remain with major support in the 62-64 area.

CL Ending Diagonal DailyCL Bear Case Daily

Crypto Markets – Counter-trend rally

To the crypto markets and the Bitcoin rally appears corrective and reversed lower from near term trend resistance. A break back below 74400-75000 support opens the door to a much larger decline. Near term inflection as it remains trapped between near term support and resistance. The risk is that the long term rally is complete.

BTC Daily semi-logBTC Weekly semi-log

That’s all for now. Have a great week and trade safe 🙂

Key events this week – US PCE inflation, Prelim PMIs March

Recap from last week: Central banks adopt a cautious approach amid an uncertain outlook.

Central bank decisions last week underscored a cautious approach to the near-term policy outlook amid rising uncertainty and a focus on persistent inflation.

The FOMC kept interest rate settings unchanged, as expected while reducing the cap on QT. The FOMC signaled it would stay on hold and was in no rush to adjust policy while growth and labor market conditions remain solid, as it waits for greater clarity on the Trump policy initiatives. The Fed Chair noted the unusually high degree of uncertainty in the near-term outlook ahead of the new policy details. For now, new projections show that inflation is expected to be more persistent with core PCE inflation projected to increase to +2.8% through 2025. However, as Powell noted, the current ‘base case’ is that core inflation is expected to fall back to 2.2% in 2026. Growth was revised lower this year, and closer to trend growth through the projection period. The unemployment rate is expected to be stable through the projection period, though rising from 4.1% currently to 4.4% by the end of this year as growth slows. Rate cut expectations narrowed, with the median remaining at two cuts for this year. The FOMC participants mirrored the elevated uncertainty with most marking up the risk weighting around their projections (source: SEP March 2025).

Powell also noted that rising uncertainty had affected sentiment among businesses and consumers, and it was not clear how this would translate into weakness in “hard data”. So far, the “hard data” has shown little effect from this falling sentiment – and it could be too early to tell. US data last week was mixed; retail sales were soft again in Feb, housing data added positively to residential investment, and manufacturing output growth was stronger than expected in Feb – possibly due to higher orders ahead of expected tariffs. The first regional manufacturing surveys for Mar showed moderating orders, output, and growth expectations, with mostly stable employment conditions. Initial jobless claims remained low/steady.

The BoE kept policy settings unchanged, remaining restrictive to “squeeze out persistent inflationary pressures”. The BoE focused on inflation risks in its deliberations – a shift from its last meeting given the higher-than-expected uptick in inflation in Feb to +3%, from +2.5% in Jan. The Committee projected that CPI inflation was still expected to rise to around 3¾% in Q3 2025. This firmer inflation appears against a backdrop of slowing growth and rising uncertainty over the impact of global trade policy since the last meeting. The minutes of the meeting indicated that while the underlying disinflation process was expected to continue, the BoE had taken a more cautious approach to its guidance;

There was no presumption that monetary policy was on a pre-set path over the next few meetings. Source: BoE Meeting Minutes, 20 Mar 2025

The BoJ kept policy settings unchanged. The assessment of current conditions and the economic outlook signaled that the BoJ is likely to maintain its stance on a gradual approach to policy normalization. Wage negotiations are producing continued stronger results, and inflation has been maintained against a backdrop of accommodative financial conditions. The Japanese National CPI data for Feb eased by less than expected, even as government energy subsidies resumed. The core CPI excluding fresh food and energy has consistently edged higher since mid-2024 and increased by more than expected to +2.6% in Feb. The BoJ Governor did express concern over whether rising uncertainties over US trade and tariff policy would impact or hinder the progress of its goals;

Ueda said last week he was “very much” concerned about the global economy in light of trade tensions. Source: Bloomberg, 19 March 2025

Outlook for the week ahead; US PCE inflation, prelim S&P PMIs for Mar, and CPI for Aus and the UK.

This week’s data will again be closely watched for signs of impact from rising uncertainty, tariffs, trade policy, and/or US spending cuts. The focus this week is on the Fed-preferred US PCE inflation data for Feb as well as the prelim S&P PMIs for Mar. US spending, income, and prelim trade and inventory data will provide a further update on the US Q1 growth run rate. Additional inflation reports for Aus, the UK, and Japan will also be important this week.

After last week’s relative calm, the US tariff announcements expected on 2 Apr, next week, could lead to a resumption of headline risk in the lead-up to that event.

Key factors to watch this week;

US PCE inflation for Feb is expected to firm. The FOMC press conference opening statement highlighted expectations for a firmer reading this month – those expectations are referenced here.

Headline PCE inflation is expected to be +2.5% over the year in Feb, unchanged from +2.5% in Jan. This would mean that PCE inflation over the month increased by +0.3% in Feb, also unchanged from +0.3% in Jan.

Core PCE inflation is expected to increase to +2.8% in Feb, up from +2.65% in Jan. This acceleration suggests that the monthly core PCE rate increased by at least +0.35% in Feb, up from +0.3% in Jan. The latest median projection from the FOMC has core PCE at +2.8% by the end of the year.

US data this week will provide a further update on spending, income, and the Advance Economic Indicators report for Feb including international trade in goods and inventories.

US personal spending for Feb is expected to increase by +0.6%, up from -0.2% in Jan.

Personal income is expected to increase by +0.4% in Feb, down from +0.9% in Jan.

The advance goods trade balance (deficit) will be closely watched after rising notably in Jan to – $153.3bn, which had accounted for much of the downshift in the Atlanta Fed growth nowcast for Q1. Growth in inventories is expected to ease to +0.4% from +0.8% in Jan.

The advance Durable Goods Orders report for Feb is expected to fall -0.7% after increasing by +3.2% in Jan.

We continue to monitor the initial claims data. So far, claims remain low, and little changed. Claims are expected to edge slightly higher to 225k last week, from 223k in the week prior.

The final revision of US Q4 GDP is expected to confirm the annualized growth rate of +2.3% at the end of last year.

A range of CPI reports for Aus, the UK, and Japan will be important;

The Aus monthly CPI series for Feb will be released this week and, while it’s not the RBA preferred report, will still be important ahead of the RBA meeting next week. Headline inflation is expected to remain unchanged at +2.5% over the year.

UK CPI will be released this week and will be important in the context of the firmer-than-expected growth in Jan. Headline CPI in Feb is expected to ease to +2.9% from +3% in Jan. Core CPI is expected to increase +3.6% in Feb, slightly lower than the +3.7% in Jan.

The latest Tokyo CPI data for Mar will provide an early guide on Japanese inflation. The Core CPI ex fresh food is expected to be unchanged at +2.2% in Mar.

The prelim S&P PMI’s for Mar will be released early this week and should provide an update on the outlook for orders, output, prices, employment, and any follow-through on weaker sentiment.

This week, the US Treasury will auction and/or settle approx. $452bn in ST Bills and FRNs, with a net paydown of -$23bn. The US Treasury will also auction the 2-Year, 5-Year, and 7-Year Notes this week – and will settle on 31 Mar.

QT this week: Approx $3.2bn of ST Bills will mature on the Fed balance sheet and will be reinvested.

More detail (including a calendar of key data releases) is provided in the briefing document – download the pdf below:

Last week, equities rallied impulsively from near term support for what we expect to be wave (a) up of a counter-trend red wave B rally. While the initial rally has stalled at 200 day sma resistance, we expect an extension higher towards the 50 day sma for wave (c) of B to potentially set up […]

Interested in accessing the MCP Market Update? Please subscribe at our Sign Up page. To learn more about this service, please visit The MCP Market Update Service.

Recap from last week: While CPI eases, tariff policy continues to sour the growth and inflation outlook.

The Feb US CPI report showed further progress on disinflation, with both headline and core CPI slowing more than expected. Headline inflation eased to +2.8% in Feb, while core CPI slowed to +3.1% in Feb, the slowest so far in this part of the cycle. These results, together with the slower monthly increases compared to last year, eased concerns about a repeat of the 2024 strong beginning-of-the-year seasonal inflation.

The underlying drivers of disinflation have flipped in the last few months. The deceleration in annual CPI in Feb was instead led mostly by core services CPI categories with shelter/owners’ equivalent rent and transportation services making the largest contribution to slower inflation. Over the last few months, core goods have no longer provided a deflationary offset.

The PPI also came in lower than expected in Feb, slowing to +3.2% in Feb, from +3.7% in Jan. However, the categories that feed into the Fed-preferred PCE inflation measure indicate that the PPI will likely make a firmer contribution to the PCE result for Feb. So far, the Cleveland Fed inflation nowcast for both headline and core PCE in Feb is +0.19% over the month, which is still marginally lower than the +0.24% core PCE recorded in Feb 2024.

While the CPI report is good news, it is a little backward-looking in the current context. Consumers, businesses, and policymakers have become increasingly focused on an inflation and growth outlook that includes tariffs and cuts to US government spending.

The US Michigan consumer sentiment report (prelim for Mar) showed that the combined effect of policy announcements has weighed further on consumer sentiment this month, with inflation expectations spiking higher, and expectations of unemployment increasing. Will the uncertain outlook prompt more cautious spending patterns? Early signs suggest that it might. One example is Delta Airlines’ cut to its sales and profit guidance for Q1, citing a recent pullback in demand across close-in, corporate, and government bookings.

Recent business surveys have also been impacted by the tariff, trade, and spending cut announcements. The latest addition was the NFIB small business survey for Feb, which showed a fall in sentiment, though still elevated, from rising caution over increased uncertainty in the outlook while reporting more widespread increases in input prices.

The Bank of Canada (BoC) meeting last week underscored the key policy challenge facing policymakers amid tariffs and a potential trade war – deriving the policy direction that balances the “downward pressure on inflation from slower growth or a weaker economy with the upward pressure on inflation from higher costs”.

The BoC cut rates for the seventh consecutive meeting. For the moment, inflation in Canada remains near the 2% target, however, the BoC expects growth to slow in Q1 as trade concerns weigh on sentiment and activity. The BoC outlook remained negative, noting that “we ended 2024 on solid footing. But we’re now facing a new crisis”.

Outlook for the week ahead; FOMC, BoJ, BoE, and SNB meetings, US data; growth outlook.

The focus for the week ahead is on key central bank meetings—FOMC, BoJ, BoE, and SNB —along with crucial US growth data. These meetings and US data will now be viewed through the lens of a growth outlook that has deteriorated in recent weeks due to the evolving tariff and trade policy landscape.

It’s becoming increasingly clear that the Trump administration views tariffs not just as negotiating tools, but as instruments for broader restructuring. Furthermore, talk of ‘detoxing’ and ‘transitioning’ the economy through reduced govt spending, coupled with the assertion that ‘corrections are healthy,’ suggests a bumpy period ahead. Uncertainty is weighing on businesses, consumers, and policymakers. The critical question now is: How substantial will the impact be from tariffs, trade policy, government spending cuts, and just rising uncertainty? This week’s data flow will be closely watched, though the combination of Feb and early Mar survey data may still only offer a partial view of any impacts.

Key factors to watch this week;

Key central bank decisions will be in focus this week. Last week, the BoC cut rates on the expectation of weaker growth in Q1 due to trade uncertainties. In contrast, the FOMC, BoE, and BoJ are expected to keep policy unchanged at their meetings this week.

The FOMC is expected to keep policy settings unchanged. In his last speech before the blackout period, Fed Chair Powell reiterated that the Fed isn’t in a hurry to shift policy, as long as growth holds up, and wants to see the net effect of Trump’s policy agenda on trade, immigration, fiscal policy, and regulation. The FOMC will submit its latest growth, inflation, labor market, and policy path projections. Any shifts in the direction of growth and inflation projections could provide some signal for whether the Fed outlook has changed. In the previous minutes, there had also been some discussion on pausing QT in the future.

The BoJ is expected to keep its policy rate unchanged, after increasing rates at the last meeting.

The BoE is also expected to keep its policy rate unchanged at this meeting. The BoE cut its benchmark rate at its last meeting, following a “gradual and cautious” path of rate reductions. While growth had been a little weaker than expected, the Committee aimed to maintain a restrictive stance as inflation risks subsided further.

The SNB is expected to cut its benchmark rate by 25bps.

Key data this week will provide a more robust update on the US growth trajectory so far in Q1. Currently, the Atlanta Fed GDP Nowcast indicates that growth has slowed early in Q1.

US retail sales for Feb are expected to rebound by +0.6% over the month, after falling by -0.9% in Jan. The Jan retail control group fell by -0.8% – this is the ,measure that feeds into the GDP result. In contrast, the Chicago Fed US retail sales nowcast suggests a downside surprise of -0.8% in Feb, with the Jan result revised up to -0.4%.

US industrial production is expected to slow to +0.2% in Feb from +0.5% in Jan.

Housing starts for Feb are expected to lift slightly to an annualized pace of 1.38m in Feb from 1.366m in Jan. Building permits are expected to slow to 1.45m in Feb from 1.47m in Jan. Amid this lackluster activity in new permits and housing starts, the weekly mortgage applications have been increased notably over the last two weeks (mostly refi’s, but also purchases) given the fall in mortgage rates.

The first US regional manufacturing surveys for Mar will be released this week and should provide some insight into any changes in sentiment and activity amid the uncertainty over trade and tariff policies.

We continue to monitor the initial claims release. So far, the trajectory of claims remains little changed. This week, claims are expected to be 222k, up slightly from 220k in the prior week.

Key data outside of the US;

The Aus labour market report for Feb will be released this week, ahead of the next RBA meeting in several weeks. Employment growth of +30k is expected to keep the unemployment rate unchanged at 4.1%.

Canada’s CPI for Feb is expected to edge slightly higher. The BoC noted some higher inflation effects due to the end of the GST pause that was implemented over the holiday period. Headline CPI is expected to increase to +2.1% in Feb from +1.9% in Jan. The core trimmed-mean and median inflation rates are expected to remain around +2.7%.

Japanese National CPI for Feb will be released after the BoJ meeting this week. The BoJ preferred measure is core CPI ex fresh food, and this is expected to ease over the year from +3.2% in Jan to +2.9% in Feb.

This week, the US Treasury will auction and/or settle approx. $591bn in ST Bills, Notes, and Bonds, with a net paydown of -$23bn. The US Treasury will also auction the 10-Year TIPS and 20-Year Bond this week – both will settle on 31 Mar.

QT this week: Approx $3.5bn of ST Bills will mature on the Fed balance sheet and will be reinvested. Approx $6bn in Notes and Bonds will mature and will be redeemed and roll-off the Fed balance sheet.

More detail (including a calendar of key data releases) is provided in the briefing document – download the pdf below: